Tax Year End Planning With A Difference

Last year’s Spring Budget was set against the backdrop of an impending general election. It complicated the process of tax-year-end planning because of the uncertainty of the election outcome. In 2016 we know there will not be a change of government, but in one area in particular, pensions, nothing else is certain. Changes announced since the election – there was another Budget in July, do not forget – also have an impact on what to consider before the 2016 Budget on 16 March.

This year Easter falls between Budget Day and the end of the tax year but, as usual, it is best that all planning is completed before the Chancellor rises to his feet. The list of issues to review in 2016 is a mix of the familiar and the new. On this occasion there is also more of a case for year-beginning planning as a result of changes due to come into effect at the start of the new tax year:

Income Tax

2015/16 saw some important changes to income tax, including:

- A £600 rise in the personal allowance to £10,600;

- The launch of what HMRC describes as the ‘marriage allowance’. This allows married couples and civil partners to transfer £1,060 of personal allowance between themselves, provided neither pays tax at more than basic rate. The allowance – worth a maximum of £212 – must be claimed as it is not given automatically;

- Two changes to the starting rate band for savings income. This was widened to £5,000 and the rate cut from 10% to zero. Alas, the changes are not as generous as they seem: the chances are you cannot benefit from the savings rate band because your earnings and/or pension cover it. But if you or your spouse/civil partner have total earnings and pension income below £15,600 a year, you will benefit if you have the right type of investment income.

As the year-end nears you should make sure that you have made the most of this trio and that you are in a position to do so for the coming tax year. That might mean re-arranging investments, closing accounts before the end of the tax year to crystallise interest or even employing your spouse/partner.

The coming tax year heralds a smaller rise in the personal allowance (to £11,000) and the arrival of two new “allowances” which are in truth more like 0% tax bands:

The Dividend Allowance

The new allowance will mean that from 2016/17 the first £5,000 of dividends you receive will be free of any personal income tax liability, regardless of your marginal tax rate. However, once the allowance is exceeded the effective tax rates are generally 7.5% higher than currently apply, as the table below shows.

Extra Tax Due on Dividends

| Tax Year

Tax Rate |

2015/16 | 2016/17 | |

| All dividends

% |

Within allowance

% |

Above allowance

% |

|

| Basic | 0 | 0 | 7.5 |

| Higher | 25 | 0 | 32.5 |

| Additional | 30.56 | 0 | 38.1 |

The personal savings allowance covers savings income – primarily interest – and is worth a maximum of £200 a year in tax savings. At today’s miniscule interest rates few people will achieve this – HMRC’s estimate is that the average benefit will be just £25 a year and that around 95% of taxpayers will no longer have to pay tax on their savings interest.

A corollary to this change is that from 6 April 2016 banks and building societies will start paying interest without deduction of tax, thereby saving HMRC a flood of small tax reclaims. National Savings & Investments will do the same, although it does already pay interest gross on some of its products. However, at least for the time being, unit trusts and OEICs that make interest distributions (eg corporate bond funds) will still have to withhold basic rate tax.

Both these new allowances mean that as part of your year-end planning you should review your investments to consider who holds what and how they are held. These allowances create some interesting new planning opportunities, not all of which are immediately obvious. For example, with the right mix of dividends and other income in 2016/17 it will be possible to receive an income of £22,000 a year without paying a penny in tax.

Inheritance Tax (IHT)

The Treasury’s income from inheritance tax rose by 60% between 2009/10 and 2014/15 and is projected to swell by another 37% over the following five years to 2019/20, despite the phased introduction of the main residence nil rate band from April 2017. The main nil rate band has been frozen at £325,000 since 2009 and, barring any new legislation, it will stay so until at least April 2021.

With no sign that house prices – one of the primary drivers for increasing IHT revenue – will fall, estate planning has become an increasingly important part of the tax-year-end exercise. There are the three main yearly exemptions to review before 6 April:

- The Annual Exemption Each tax year you can give away £3,000 free of IHT. If you do not use all of the exemption in one year, you can carry forward the unused element, but only to the immediately following tax year, when it can only be used after that year’s exemption has been exhausted. For instance, if you did not use the annual exemption in the last tax year, 2014/15, you can still use it by 5 April 2016 (a Tuesday – what matters for cheques is the clearing date), but only once you have fully used the 2015/16 exemption. Thus a gift of up to £6,000 (£12,000 for a couple) can escape IHT.

- The Small Gifts Exemption You can give up to £250 outright per tax year free of IHT to as many people as you wish, so long as they do not receive any part of the £3,000 exempt amount. The more grandchildren, nieces and nephews you have, the more useful is this exemption.

- The Normal Expenditure Exemption The normal expenditure exemption is potentially the most valuable of the yearly IHT exemptions. Any gift is exempt from IHT provided that you make it regularly, it is made out of income (including ISA income, but not from any capital) and its does not reduce your standard of living. No cash limits apply to this exemption. You can gift dividend or other investment income which would otherwise usually be reinvested, with the normal expenditure exemption covering the gift. Next tax year’s dividend allowance could increase your scope for using this exemption by cutting your dividend tax bill.

Capital Gains Tax (CGT)

After two consecutive years in which the FTSE 100 has fallen, the issue of CGT might seem academic, but it is not. For a start, while the FTSE 100 fell in 2014 and 2015, the FTSE 250 rose in both years and longer term there are still gains about from UK shares.

Regular use of your CGT annual exemption (now £11,100) is one way to avoid the situation where gains built up over a period of years lead to a tax bill for rebalancing your portfolio, drawing out some cash or, if you have a direct share portfolio, accepting a takeover bid. The 2015/16 annual exemption could save you nearly £3,100 in tax if you pay tax at more than basic rate. If you cannot avoid capital gains tax, then it pays to watch the timing of your gains:

- A gain realised on 5 April 2016 will mean tax payable on 31 January 2017.

- A gain realised on 7 April 2016 will move the tax payment date to 31 January 2018.

The timing of when you realise any losses also warrants scrutiny, a point often overlooked as there is no tax to pay. The general rule is that your losses are set against gains made in the same tax year before the annual exemption is applied. Ideally therefore, you should avoid making losses in the same year as that in which you realise gains, unless your total gains exceed the annual exempt amount.

Pensions

2015/16 marked the beginning of pension flexibility for money purchase schemes. In the first six months following the reform over 380,000 pension arrangements were accessed under the new rules of which nearly 240,000 were fully encashed, according to the Financial Conduct Authority. The introduction of flexibility, radical though it was, is by no means the end to important pension changes.

We already know that on 6 April:

- The lifetime allowance, which effectively sets the maximum tax-efficient value of your total pension benefits, will be cut by 20% to £1,000,000. That may still sound a significant sum, but for a 65 year old wanting an inflation-proofed pension, £1m will only provide an inflation-proofed income of about £2,770 a month (before tax) at current annuity rates – and that with no provision for a widow(er)’s benefit.

- Two new transitional protections will be introduced to help those hit by the lifetime allowance reduction.

- The annual allowance, which effectively sets the maximum tax-efficient total pension contributions in a tax year, will be subject to tapering down to a minimum of £10,000 if you have a high income (broadly speaking over £110,000 after deducting any personally made pension contributions).

Even more significant is what we currently do not know. In July the Chancellor issued a consultation document on the future tax treatment of pensions. A report back was expected at the time of the Autumn Statement, but has been deferred until the Budget. The rumour machine is increasingly pointing to a reform which will replace full income tax relief with a flat rate relief between 25% and 33%. That could be good news if you are a basic rate taxpayer – it depends what else emerges – but it would obviously be bad news if you pay tax at the higher or additional rates.

A review of your maximum pension contribution options now is a clear priority if you pay 40% or 45% tax, or if the new lowered lifetime allowance could affect you. In theory it is possible, by combined use of the rules on carry forward and pension input periods, to contribute up to £180,000 with full tax relief in the current tax year, if your circumstances permit. In any event, 2015/16 is your last opportunity to carry forward up to £50,000 of unused annual allowance from 2012/13.

The question of whether to claim one of the new transitional reliefs must be put on hold for now, as the final details and claim procedures are unlikely to emerge until the summer.

Individual Savings Accounts (ISAs)

The standard ISA contribution limit for 2015/16 is £15,240, as it will be for 2016/17. The limit applies for total ISA investment, so investment can all be in the stocks and shares component, all in cash or a mix of the two (usually with different providers). For the Junior ISA, the limit for both tax years is £4,080, with the same ceiling applying to Child Trust Funds.

Cash ISAs have had a question mark hanging over them for some years, given the very low interest rates currently on offer. For example, at the time of writing the best rate available was 2.55%, but only for a five year fixed term (and a lot can happen in half a decade). In the coming tax year, the arrival of the personal savings allowance (see ‘Income Tax’ above) will further test the relevance of cash ISAs. The Treasury has effectively acknowledged this by making two changes to the ISA rules from 6 April 2016:

- It will be possible to withdraw money from a cash ISA and replace it within the same tax year without the replacement counting towards the contribution limit.

- A new, quasi-cash ISA, the Innovative Finance ISA, will come into being, which will allow investment in peer-to-peer (P2P) lending. This should offer higher interest rates, but without the capital security of the traditional cash ISA.

The new dividend allowance poses similar issues for the stocks and shares ISA variant, as you may no longer need to invest via an ISA to avoid extra tax on dividend income.

The net result of these various reforms is that the normal year-end mantra of “top up your ISA” should now be replaced with “review your ISAs”. Maximising your ISA contributions could still make sense, but the role ISAs play in your overall planning should be examined first. For instance, the personal savings allowance could mean that you can switch a cash ISA to a stocks and shares ISA and instead receive interest tax-free from directly held deposits.

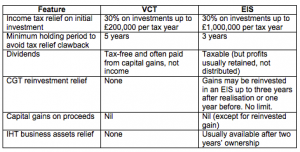

Venture Capital Trusts (VCTs) and Enterprise Investment Schemes (EISs)

The tax laws governing VCT and EIS rules are regularly amended and the latest changes, most of which took effect last November, have altered the risk profile of both schemes. The revisions were driven by earlier reforms to EU state aid rules, which aimed to focus tax-incentivised investment more sharply on younger, smaller companies. For example, the new rules place age limits on the companies in which VCTs and EISs may invest. They also effectively ban investment in management buy-outs (MBOs), which have long been a popular (and rewarding) choice for some of the larger generalist VCTs.

Broadly speaking, VCTs and EISs will now have a smaller and potentially riskier pool of companies in which to invest. Some managers are holding back from making any new offers this tax year end while they review and, in some cases, rework their investment strategy. The corollary is that supply might be limited and attractive offers could sell out very quickly – one leading VCT launched a £10m share offer on 11 January, only to close it, fully subscribed, four days later. Demand is expected to be high for VCTs and EISs this year end because of the increasing constraints on pensions and the well-publicised problems faced by users of aggressive tax avoidance schemes.

As a reminder, the current tax benefits of VCTs and EIS are:

ACTION

The Budget is now less than seven weeks away, so do not delay your year-end/year- beginning planning, particularly on the pensions front.

Call us now to arrange for a comprehensive tax planning review. The sooner you contact us, the sooner we can begin work on your strategy and decide on actions for this tax year and the early part of next tax year.

AUTOMATIC ENROLMENT: RAMPING UP TIME

At the start of the year, the Pensions Regulator (TPR) issued a press release reminding small employers that auto enrolment in workplace pensions was rapidly arriving in their sector of the business market. Hitherto, the auto-enrolment procedure has been working its way down in terms of employer size, starting with the largest businesses back in October 2012. By September 2015 over 60,000 employers had been through the auto-enrolment process – an average of about 20,000 a year. However, TPR calculates that in 2016 alone there will be up to 500,000 employers who have to deal with the workplace pension rules for the first time.

The huge jump in numbers during this year threatens to create problems and backlogs, particularly for employers who have not followed TPR’s advice to start planning at least a year in advance of when they have to begin operating auto-enrolment.

ACTION

If your business is yet to enter the automatic enrolment process, do not think that you can afford to procrastinate until the last moment or wait until the Pensions Regulator starts to send out compliance notices, yet alone fixed penalty notices. The sooner you start, the less you expose your business to additional costs, regulatory hassle and reputational risk.

For an analysis of your business’s automatic enrolment options, please talk to us…now.

Past performance is not a reliable guide to the future. The value of investments and the income from them can go down as well as up. The value of tax reliefs depend upon individual circumstances and tax rules may change. The FCA does not regulate tax advice. This newsletter is provided strictly for general consideration only and is based on our understanding of law and HM Revenue & Customs practice as at January 2016 and the contents of the 2015 Autumn Statement and Finance Bill 2016 draft clauses. No action must be taken or refrained from based on its contents alone. Accordingly no responsibility can be assumed for any loss occasioned in connection with the content hereof and any such action or inaction. Professional advice is necessary for every case.

Leave a Reply