The Autumn Statement 2016

This year’s Autumn Statement was much awaited as the first set piece for the new Chancellor, Philip Hammond. In the days immediately following his appointment Mr Hammond had spoken about the possibility of a “fiscal reset” and November 23 was eagerly anticipated as the time when the meaning of the phrase would be revealed.

In the event, there was little sign of a reset, beyond £122bn being added to the projected numbers for government borrowing through to 2020/21. That jump in debt was partially of Mr Hammond’s own creation and in part down to the impact of Brexit on the calculations made by the Office for Budgetary Responsibility (OBR). Either way £122bn of more government IOUs means that tax cuts, other than those already announced, have been pushed further into the 2020s.

Mr Hammond – “Spreadsheet Phil” as the Financial Times calls him – has a more restrained style than his predecessor, a fact which came through in the measures he announced. In terms of tax and spending, there were no rabbits-out-the-hat, but the Chancellor did manage to surprise MPs and pundits alike by announcing he would move the Budget onto an Autumn cycle from November 2017, meaning that we can look forward (or otherwise) to two Budgets next year and an Autumn Budget only from 2018 onwards.

The more interesting measures that were announced in the final (for now) Autumn Statement include:

Fringe benefits attacked

For many years there has been a growing trend among employers to offer their employees a pick-and-mix choice in the way they are rewarded. ‘Flexible remuneration’ has meant that employees have been able to swap cash pay for any of a range of fringe benefits, from more pension contributions, through gym club membership and company cars to mobile phones and payment of school fees.

The driving force behind all these salary sacrifice schemes has been savings in tax and/or National Insurance contributions (NICs). In some instances – such as if you give up pay for a new iPhone 7 or gym membership – all tax and NIC liability is extinguished because the benefit is exempt. From the Chancellor’s viewpoint the corollary to this disappearing trick is that what you and your employer avoid paying equates to revenue that the Treasury does not receive.

In his Spring Budget Mr Osborne announced a consultation on the treatment of fringe benefits and his successor has predictably followed up with new measures from April 2017. Broadly speaking, these will mean you are taxed (and your employer charged NICs) on the salary you give up or the value of the benefit, whichever is higher. There are transitional provisions for arrangements in place before 6 April 2017 and a handful of specific exemptions. The most important is that exchanging pay for pension contributions will not be caught.

Pensions

The usual rumours that higher rate tax relief on pension contributions was for the chop once again proved unfounded. However, the Chancellor did announce a further tightening of the tax relief screw, with a 60% reduction in the money purchase annual allowance (MPAA) to £4,000 from 2017/18. This allowance only applies if you are making pension contributions having drawn any income using the pension flexibility rules.

Interestingly, the consultation document which the Treasury published on the revised MPAA said “The cost of tax and National Insurance contributions relief on pension savings is one of the most expensive sets of relief offered by the government. In 2014 to 2015 this cost around £48 billion, with around two thirds of the tax relief going to higher and additional rate taxpayers.” Draw your own conclusions…

Shortly after the Autumn Statement it was confirmed that the new single-tier pension and the old basic state pension (payable if you reached state pension age before 6 April 2016) will both rise by 2.5%, to £159.55 a week and £122.30 a week respectively. Other state pension benefits will rise by 1%, in line with CPI annual inflation to September. The 2.5% rise was thanks to the “triple lock”, which sets a floor increase at that level. To judge by recent comments, including the Chancellor’s, the cost of meeting the triple lock could well mean it disappears after the end of this Parliament.

Value added tax

A change to the VAT flat rate scheme (FRS) was announced, to take effect from next April following consultation over the holiday period. The proposals received little attention, but could reduce your earnings if you are FRS VAT-registered, self-employed (or operate as a limited company) and your business is primarily about supplying labour, i.e. the business buys few goods (not services). Many of those caught by the change will be acting as consultants: some will see their income drop by 5% because of the extra flat rate VAT they will have to pay.

Anti-avoidance

There was the usual raft of anti-avoidance measures announced including a consultation on whether to make access to licenses or services for businesses conditional on tax registration. The new Chancellor also confirmed that he would implement the proposals from his predecessor to create a new legal “requirement to correct” a past failure to pay UK tax on “offshore interests” within a specified timeframe. This is a precursor to the full implementation of the Common Reporting Standard (CRS) in September 2018, which will see over 100 countries automatically exchange taxpayer information.

Insurance premium tax

Insurance Premium Tax (IPT) was launched by the last Chancellor to have Autumn Budgets, Ken Clarke, in November 1993. IPT started life at a rate of 2.5%, but has since reached 10% following a series of rises. Mr Hammond copied his predecessor by adding another increase, this time of 2% to 12%, from 1 June 2017. IPT is one of the preferred tax increases for this government as it is outside the ‘triple lock’ on income tax, NICs and VAT, but can still raise useful amounts of revenue. IPT does not apply to life assurance or income protection, but covers just about everything else, including medical, car, pet and household insurance.

ACTION

The final Autumn Statement showed that the new Chancellor has no room for tax giveaways and is still seeking ways fill the Exchequer’s coffers.

The end of the tax year (and, before that, the next Budget) are not that far away. With continued rumblings about the cost of higher rate relief on pension contributions, reviewing your retirement planning should be a key area for your tax year end planning.

DEPOSIT PROTECTION SET TO CHANGE

At the start of 2016, the limit for deposit protection under the Financial Services Compensation Scheme (FSCS) was cut by £10,000 to £75,000. By the end of January 2017, it is almost certain to be back at £85,000. The reason embraces two of this referendum year’s most contentious items: EU law and the euro.

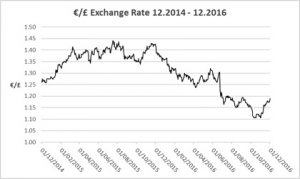

The European Deposit Guarantee Schemes Directive (EDGSD) sets a minimum level of €100,000 or the local currency equivalent on deposit protection. For non-Eurozone EU members, such as the UK (for the time being), the Directive requires a reassessment of their local currency cover level every five years, taking account of prevailing exchange rates. The UK’s last review was in Summer 2015 when, as the graph shows, £1 would buy a little over €1.40. The previous limit had been based on a much lower exchange rate, hence the £10,000 cut that, thanks to transitional measures, mainly took effect in January 2016.

To put it mildly, a lot has happened since. One of the main events – the vote for Brexit – prompted a sharp fall in the pound against almost every currency. The drop against the euro was from around €1.30 on 23 June to just over €1.10 in October, although sterling has since recovered to nearly half its lost ground. Fortunately, the EDGSD was designed to cater for such currency volatility. In addition to the standard quinquennial review period, the Directive requires an adjustment to be made following “unforeseen events” (!)

In November, the Bank of England issued a consultation paper proposing to send the cover level back up to £85,000. To a large degree, the consultation is a formality as there will be no opposition to the increase, due to take effect on 30 January 2017. It will make life a little easier for those with large deposits – a £250,000 deposit will need to be spread across three banks rather than four to gain full protection.

ACTION

This is a welcome, if minor move. Depositor protection still matters – witness the efforts underway at the time of writing to find an institution to take over the struggling Manchester Building Society, which has some members with £75,000+ deposits.

If this increase matters to you, then you may be holding too much cash, probably earning a sub-inflation interest rate. Why not talk to us about assessing the amount of liquidity you need and the options for earning more income from your capital?

TAX CHANGES DUE FROM APRIL 2017

One of the less endearing habits of Chancellors, regardless of political hue, is to announce tax changes which are deferred for a year or even more. This might be to delay a cost to the Exchequer or in the hope that a tax increase gets forgotten. Mr Hammond served up some deferred measures, but for April 2017 there are two from his predecessor worth remembering:

Inheritance tax residence nil rate band

The residence nil rate band (RNRB) was promised in the 2015 Conservative manifesto, where it was described as ’increasing the effective Inheritance Tax threshold for married couples and civil partners to £1 million, with a new transferable main residence allowance of £175,000 per person’. It sounded simple at the time, but the legislation proved to be hugely complex. The chairman of the Treasury Select Committee was prompted to write to the Chancellor saying ’Tax rules should aim to be simple, fair and clear. I am concerned that the RNRB announcement meets none of these tests.’

The RNRB starts from 6 April 2017 and initially is worth only £100,000. It will rise by £25,000 a year to reach £175,000 in 2020/21, shortly before the next election is due. Very broadly speaking the RNRB is equivalent to an extra £100,000 on the nil rate band, but it only applies to residential property (or assets replacing that property on downsizing) passing to lineal descendants on death. The RNRB is subject to taper for estates over £2m and, like the ordinary NRB, any unused element can be effectively inherited by a surviving spouse or civil partner.

Tax relief on buy-to-let mortgages

In the first Budget after that 2015 election which the Conservatives won, George Osborne announced two measures aimed at cooling the buy-to-let market. The first, the replacement of the 10% wear and tear allowance, took effect last April. The other, a four-year phased reform of the tax relief on mortgage interest, begins from 2017/18. In the first stage, a quarter of interest payable will cease to be allowable against rental income and instead the borrower will receive a 20% tax credit on that portion of interest.

This is an unwelcome two-edged sword if you are a buy-to-let investor:

- If you pay tax at more than basic rate, then the tax relief you receive on interest payments will be less. Ultimately, most higher rate taxpayers will see their mortgage interest tax relief halve by 2020/21.

- Because the interest deduction against rental income is being tapered away, your total income (including rent net of expenses) will increase. This could mean extra tax because you move into a different tax band or the extra income takes you over a tax threshold, eg the £50,000 ceiling above which child benefit is effectively taxed.

ACTION

It is generally best to plan for tax changes before they take effect, rather than once they are in force.

The RNRB’s arrival is a good reason to review your estate planning. For example, it may no longer make sense to pass everything to a surviving spouse on first death. Similarly, the reduction in buy-to-let interest relief should prompt a re-assessment of the structure of property ownership and even whether the investment remains worthwhile, especially as interest rates could rise from current low levels just as tax relief drops.

AUTO-ENROLMENT FINES ACCUMULATE

Automatic enrolment in workplace pensions started in October 2012 and is now reaching the final stages, with the last employers with workforces of under 30 individuals and new employers since April 2012 having to comply. By the end of September 2016 over 250,000 employers had completed the automatic enrolment process and more than 6.7m people had started saving into workplace pensions. However, the path has become rather less smooth as the focus has moved to the smallest employers.

Warnings and Penalties Escalate

In the July-September quarter of 2016, the pensions regulator (TPR) served over 15,000 compliance notices to employers, requiring them to correct errors in the automatic enrolment process. In the previous three years nine months less than 11,000 notices had been served.

It was a similar story for fixed penalty notices of £400 levied for failure to comply: over 3,700 were issued in the third quarter, more than the total number that had been issued from October 2012 to June 2016. Escalating penalty notices – which can run up to £10,000 per day – also had a boom time, with TPR sending out 576 notices against a total of 165 in all the previous quarters.

And in 2018…

Once the automatic enrolment process reaches an end, the next challenge will be an increase in the level of minimum total contributions. This is currently 2% of band earnings (those between £5,824 and £43,000), of which the employer has to pay at least 1%. From April 2018, the total will become 5%, with an employer minimum of 2% – in other words a tripling of contributions for most employees. A year later there will be a move to an 8% total, with the employer paying at least 3%.

ACTION

The last round of auto-enrolment will see heavy demand for advice as procrastinating employers realise the time has come to act.

If you have not yet prepared for auto-enrolment, talk to us as soon as possible about your options.

Past performance is not a reliable guide to the future. The value of investments and the income from them can go down as well as up. The value of tax reliefs depend upon individual circumstances and tax rules may change. The FCA does not regulate tax advice. This newsletter is provided strictly for general consideration only and is based on our understanding of law and HM Revenue & Customs practice as at December 2016 and the contents of the Autumn Statement 2016. No action must be taken or refrained from based on its contents alone. Accordingly no responsibility can be assumed for any loss occasioned in connection with the content hereof and any such action or inaction. Professional advice is necessary for every case.

Leave a Reply