LISA No Substitute For Pension

The Lifetime ISA, which everybody except the Treasury calls LISA, was one of Mr Osborne’s 2016 Budget surprises. It looked very much like the replacement for pension plans which had been floated by various organisations in the run up to March.

LISA Basics

The main facts about LISAs, as they have emerged so far, are:

- They will come into being from April 2017 and will be available only to the under-40s;

- The maximum contribution will be £4,000 per tax year, which will count towards the overall ISA limit (£20,000 from next April);

- The government will pay a 25% bonus on the contribution made in a tax year at the end of that year, provided the subscription is made before age 50;

- The bonus (plus any interest or growth on it) will be clawed back and a 5% penalty levied on withdrawals unless they are made either:

- From age 60 onwards, or

- For the purchase of a first home (subject to a maximum value of £450,000); a

- The tax treatment will be the same as for existing ISAs, meaning that no UK income tax and no capital gains tax will be payable.

Smoke and Mirrors

The 25% bonus has the same effect as basic rate tax relief for a pension contribution – but sounds better. If you are a basic rate taxpayer making your own contribution and receiving the bonus, the LISA is superior to a pension because at 60 you can draw 100% of the LISA’s value as a tax-free lump sum, whereas only 25% of a pension plan is tax-free, with the other 75% taxable.

The mathematics are not as simple if your employer contributes to your pension and/or if you pay tax at more than basic rate (you do not get a bigger LISA bonus, but you do receive more tax relief on a pension contribution). Automatic enrolment into workplace pensions complicates matters further.

If you have to make a choice, then with very few exceptions your automatic enrolment pension contribution will be more valuable than a personal LISA contribution. The reason is the employer’s mandatory pension contribution which, as a general rule, will be contingent on you making a contribution.

In theory employers will be able to contribute to LISAs, just as they can to ISAs. However, such contributions have to be treated as pay and are therefore subject to income tax and National Insurance contributions.

An Omen?

The most worrying aspect of the LISA is that it will set up an alternative savings vehicle to pensions. The pre-Budget leaks suggested that Mr Osborne had abandoned his planned radical reform of pension taxation primarily because he did not want to unsettle the electorate ahead of June’s referendum. It is quite possible to imagine that in a future Budget Mr Osborne (or his post-Brexit successor) will announce that the age 40 limit for LISAs has been scrapped…along with income tax relief for pension contributions.

ACTION

The message from LISA is that while full income tax relief on pension contributions is available in 2016/17, its long-term future remains in doubt.

Now is the time to review your pension contributions and take advantage of the carry forward rules. To see how much you could contribute, talk to us as soon as possible.

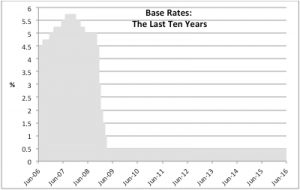

The Bank of England’s base rate has now been fixed at 0.5% for over seven years. However, that does not mean other interest rates have remained static. In particular, savings rates have been dropping to microscopically small levels.

NS&I Join the Cutters

One of the most recent rate cutters was National Savings & Investments (NS&I), whose rate reductions will mostly take effect during June. Two of NS&I’s more popular offerings, the Income Bond and the Direct ISA, will have their rates cut from 1.25% to 1.00%. Viewed another way, that is a drop of one fifth in the interest payable. NS&I are also reducing the prize fund interest rate on Premium Bonds, from 1.35% to 1.25%.

The prize fund cut has forced two changes to the structure of bond prizes. Firstly, the odds of a win in the monthly draw will get worse, moving out from 26,000:1 to 30,000:1. The second change is a revamping of the prize mix, with fewer of the £500 and over prizes. If you win in a monthly draw after the change, over 93% of the time your prize will be just £25.

NS&I are normally not near the top of the league table for interest rates. In part NS&I blames the falls on the fact that it had become too competitive because the banks and building societies have been axing their rates. At the time of writing (May 2016) the best instant access rate was 1.45%, while even the top five year fixed term rate was only 2.70%.

Going lower?

In theory rates could go lower – Japan and the Eurozone are both experiencing the bizarre world of negative interest rates in which some depositors pay interest and borrowers can earn interest. So far Mark Carney, the Governor of the Bank of England, has ruled out negative interest rates, but then so did the governor of Japan’s central bank, until he changed his mind.

Press reports in May suggested that the Bank of England could reduce interest rates if the UK votes for Brexit, although other commentators have said the same result will force the Old Lady to raise rates to protect the pound. If there were a rate cut, then negative territory becomes a greater possibility for the UK.

Alternatively…

Strangely, while savers’ interest rates have been going south, the dividend yield on UK shares has been increasing. As at early-May 2016, the UK stock market had an average dividend yield of 3.79%, 0.6% higher than twelve months previously. And do not forget that in 2016/17, the first £5,000 of dividends you receive are free from tax, regardless of your marginal tax rate. The personal savings allowance only exempts £1,000 of interest from tax (if you are a basic rate taxpayer) or £500 if you pay tax at 40% (additional rate taxpayers receive no allowance).

ACTION

There is a wide range of UK equity income funds to choose from although, as ever, there is more to selection than just going for a single number – the highest yield. Some funds have a much better track record for growing their income than others, an important factor when some big names, like Tesco and Barclays, have cut pay outs to investors.

To gain an insight into the best-of-breed UK equity income funds, talk to us. The income will be a lot more interesting than that from NS&I.

When asked why he robbed banks, the US criminal Willie Sutton is said to have replied “because that’s where the money is.” A similar type of response is often applied to the issue of raising tax revenue: tax the rich because, by definition, that’s where the money is. The argument has been supported in the USA by growing income inequality – hence the campaigns against “the 1%” who, on some accounts, globally own as much as all of the other 99%.

A UK Perspective

In this country, the well-respected Institute for Fiscal Studies (IFS) has been examining the pattern of tax raising and how it has – and will – change by 2020. The Institute’s findings may come as a surprise to the tax-the-rich lobbyists, but may not to you, especially if you already pay tax at more than basic rate.

The IFS found that up until the financial crisis in 2007, the proportion of income tax paid by the top half of taxpayers had increased, but mainly because their earnings were rising faster than the population’s as a whole. The booming financial sector – think bank bonuses – was an important factor. However, the picture of increasing income tax share did not change once the crisis hit. As the IFS notes, what had happened simply as a result of earnings inertia until 2007 became a deliberate government policy thereafter. For example:

- The top rate of tax was increased to 50% in 2010/11 (and subsequently reduced to 45%).

- Child benefit was brought into tax for those with incomes above £50,000 and child tax credit restricted to low/medium earners.

- Pension tax reliefs were systematically cut back, with the latest reduction to the standard lifetime allowance having just taken place at the beginning of this tax year.

- The starting point for higher rate tax has been regularly manipulated with the result that the 2016/17 threshold (£43,000) is still lower than the figure which applied seven years ago (£43,875 for 2009/10).

- The personal allowance has been phased out for those with incomes of over £100,000.

- Tax thresholds which affect the wealthier element of the population have been deliberately frozen – the additional rate of tax still starts at the same level as it did when launched, as does the taxation of child benefit and the phasing out of personal allowances. Similarly, the inheritance tax nil rate band of £325,000 has also been frozen since April 2009, with part of the justification for the freeze being reform of long-term care funding which was subsequently deferred for four years, shortly after the election.

The current and previous government made much of the increases to personal allowances and these have been costly in terms of Exchequer revenue. The IFS says that 56.2% of the adult population were taxpayers in 2015/16 against 65.7% in 2007/08. Even so, that smaller proportion is still producing much the same share of the Treasury’s income as it did eight years ago.

The Higher Rate Threshold

The Chancellor has a target of raising the higher rate threshold to £50,000 by the end of this Parliament (ie 2020/21). However, even if he introduced that figure today, it would still not match what price indexation – the old basis of increases – would have produced. There is some sleight of hand here, too. The higher rate threshold also sets the upper limit for full rate National Insurance contributions (NICs). Thus, if you are a higher or additional rate taxpaying employee, the 20% tax saving that an increase in the higher rate threshold gives you is halved once you take account of the fact that you will be paying 12% NICs on the increase element rather than 2% – and now getting no additional state pension benefit for doing so.

ACTION

The rich – and not so rich – are paying more tax and, whatever the politicians say, that will continue to be the case.

The corollary is that tax-planning has become all the more important. If your tax plans have not been reviewed in the light of all the recent tax developments, you could be paying even more tax than you need to.

The latest figures from HMRC – admittedly for 2012/13 – show that there were 940,000 company cars on the UK’s roads. Their taxation is one of the more curious aspects of Budget announcements. Chancellors of both hues have tended to announce changes (aka increases) in their Budgets that do not take effect for several years. For example, in the March Budget Mr Osborne revealed consultation plans for 2021/22 and beyond – after the next election.

Delay and Forget

The delayed implementation may be a ploy, on the basis that it will be long forgotten by the time it arrives as a tax code adjustment. Nevertheless, the net effect is still for tax increases on a year-by-year basis. The latest round of changes, which were finalised in the 2013 Budget, have added 2% to the ‘scale benefit’ for most cars. For instance, the scale benefit on a BMW 320d has risen from 19% to 21%, equivalent to an increase of more than a tenth in the tax payable. In the case of the BMW, as with other diesels, the benefit had been due to fall for 2016/17 because the original intention was to scrap the 3% diesel supplement. However, in the wake of the VW defeat device scandal (and the Treasury’s constant need for more income), the Chancellor decided that the 3% levy would remain.

More Next Year

In 2017/18 another 2% will again be added to most scale benefit numbers, although as now the ceiling will remain at 37% for the highest emission vehicles. 2018/19 will see the same hike again, taking that BMW 320d’s scale benefit up to 25%.

ACTION

If you are entitled to a company car, the ever-increasing tax scales may mean you would be better off taking more pay or other benefits as an alternative. Certainly, if your employer provides “free fuel” you should look very carefully at whether that is worthwhile: the tax on this perk has gone up, even as pump prices have been dropping.

Talk to us about your options: a company car is just another aspect of remuneration and you may be surprised how much you could save by tweaking your overall pay package.

THE PENALTY SPOT

Fancy paying a fine of £23,000? Bar £100, that is what it cost Swindon Town Football Club in fines from the Pensions Regulator (TPR) for persistently ignoring the club’s responsibilities as an employer under the automatic enrolment pension provisions. Swindon managed to score quite a crop of own goals, but it is not alone in attracting TPR’s attention.

According to the latest quarterly statistics from the regulator in the first quarter of 2016:

- Over 3,000 compliance notices were issued, bringing the total since October 2012 to nearly 8,000;

- 806 £400 fixed penalty notices were issued; and

- 96 escalating penalty notices were issued. These can be up to £10,000 per day.

As had been widely expected, the smooth roll out of automatic enrolment by large and medium-sized employers has become a lot bumpier as small and micro-employers have reached their ‘staging dates’. The sheer number of employers involved meant an increase in penalties was inevitable, but the jump suggests that there are deeper problems.

ACTION

If your business has yet to enter the automatic enrolment process, take the advice of the Pensions Regulator: “Employers should not ignore their duties”.

For help in dealing with your business’s automatic enrolment requirements, please talk to us as soon as possible.

Past performance is not a reliable guide to the future. The value of investments and the income from them can go down as well as up. The value of tax reliefs depends upon individual circumstances and tax rules may change. The FCA does not regulate tax advice. This newsletter is provided strictly for general consideration only and is based on our understanding of law and HM Revenue & Customs practice as at June 2016 and the contents of the Finance (No. 2) Bill 2016. No action must be taken or refrained from based on its contents alone. Accordingly, no responsibility can be assumed for any loss occasioned in connection with the content hereof and any such action or inaction. Professional advice is necessary for every case.

Leave a Reply